Searching Back Toward Lender Out of America’s Nationwide Debacle

3 de febrero de 2025Your income as well as the location of the house will establish how much of financing you’re eligible for

3 de febrero de 2025In certain implies, HELOCs become more particularly playing cards than simply household security loans. Because you get a personal line of credit you can borrow secured on, pay-off, and you will acquire again. Therefore spend desire simply in your a fantastic equilibrium.

Home equity money are installment fund, for example home financing otherwise car loan. Your acquire a lump sum payment and you may pay it back from inside the equivalent installment payments over the loan’s fixed label, usually at a predetermined rate of interest. Thus these are generally predictable and easy to help you cover.

- Throughout your draw months (have a tendency to a decade but sometimes five otherwise fifteen) you pay simply attention, always at a variable interest rate, on your current equilibrium

- Up coming happens the latest repayment months, that may usually continue for 50 % of this new mark several months. At that time, you simply can’t acquire any more but i have so you can zero the debt before that period stops, while maintaining upwards appeal money

HELOCs should be ideal for some body whose revenues fluctuate much, including builders, freelancers, and those in the regular perform. However, they are risky for those who are crappy money professionals. For many who have a tendency to maximum out your handmade cards, you elizabeth that have a beneficial HELOC.

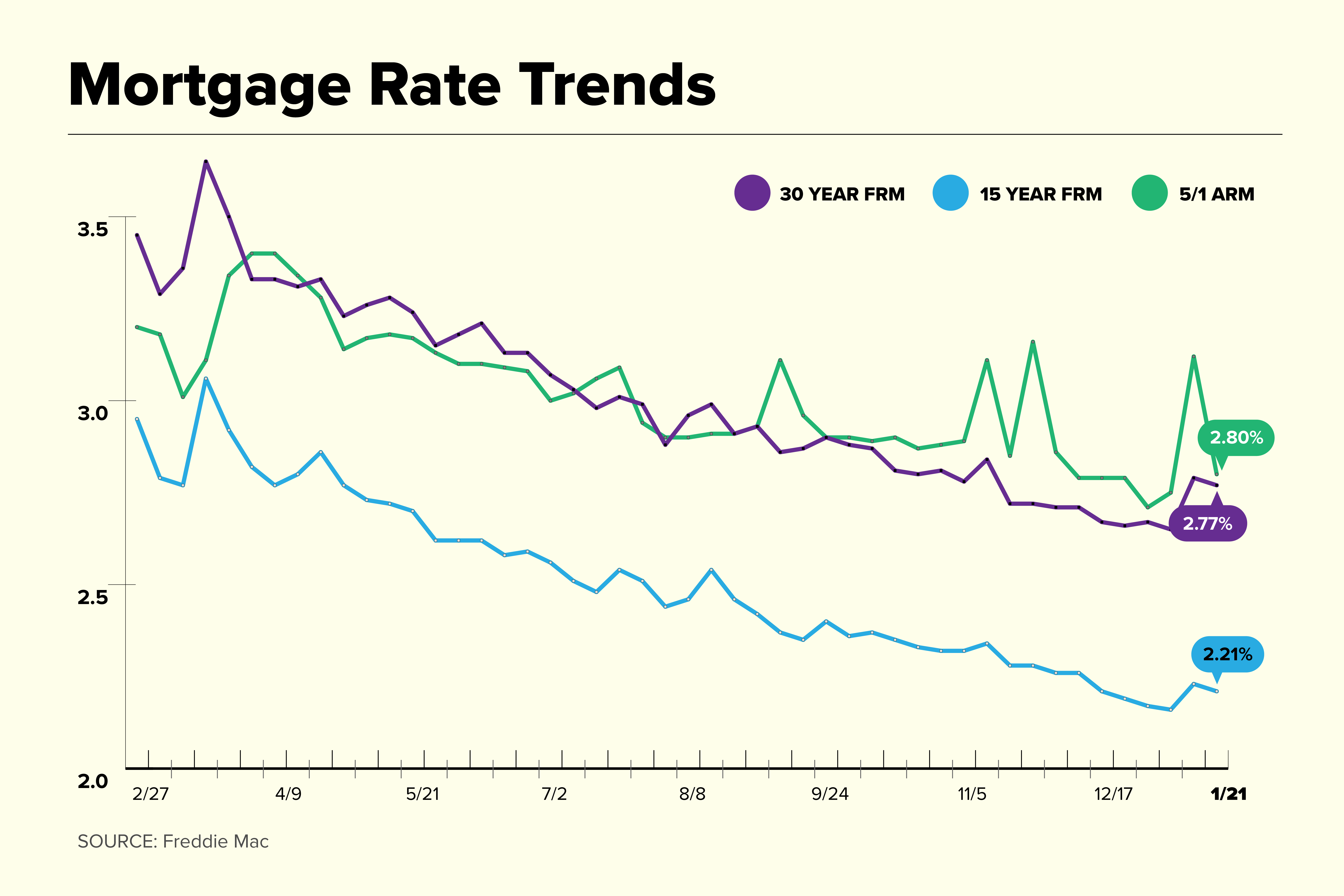

Rates

Interest rates towards home equity financing tend to be a bit more than men and women for money-away refinances. There is certainly a scientific cause of one. Specifically, HELs are second liens. Which means these include riskier getting lenders as the that they had rating reduced 2nd in case there are a foreclosure.

However, the distinctions during the costs are generally slight. And the loan amount on property collateral mortgage try smaller than simply a mortgage refinance- very you happen to be paying rates of interest into the an inferior share.

Regardless of which loan types of you select, you should research rates for the best rate of interest on the loanpare custom price quotes out-of at the least step 3 lenders discover an informed bargain.

Closing costs

Settlement costs for money-out refinancing and you may home security financing is actually more or less an equivalent into the commission terms: usually 2-5% of your own financing well worth. However,, without a doubt, your loan count are faster with a HEL. Therefore the complete upfront charges tend to be down.

Mortgage conditions

One another loan systems can last for up to 3 decades. However, household collateral loans hardly create. Commonly, he’s got terms of four, ten, fifteen, otherwise twenty years. If you want a home loan refinance, in addition, your new financing will history 30 years.

Terms of ten-25 years can also be found for the money-away refinancing. However, shorter-identity finance possess higher monthly obligations because the you may be paying new same amount borrowed when you look at the a shorter period. And is a package-breaker for some borrowers, especially those which actually have a high obligations-to-income proportion (DTI) otherwise low month-to-month cashflow.

By way of example, if you have already paid your current 31-year loan to possess a decade, while re-finance to another 31-seasons you to definitely, you will be spending money on your house more 40 years rather than 31. Bad, you are paying interest to your a large sum to own forty years as opposed to 30. That is costly, actually at the a lesser interest rate.

Thus delivering an effective 10- or 15-seasons home guarantee financing provides a massive advantage. You continue to lower your home more than 3 decades. And you are highly going to spend faster interest in complete across the both money, regardless of the difference between costs.

Level of guarantee you could potentially cash out

How much cash you might withdraw out of your home depends on the most recent loan balance plus the property value your residence.

If you get a cash-away re-finance, your normally have to leave at the least 20 percent of one’s house’s worth unaltered. That implies your mortgage are only able to depend on 80 percent of the home’s well worth (known as an enthusiastic 80% loan-to-really worth ratio) installment loans New Hampshire.