The different costs use predicated on whether it’s the first have fun with of the Va loan guarantee (2

15 de octubre de 2024Jess looks like separating with Russell as his or her dating enjoys no welfare

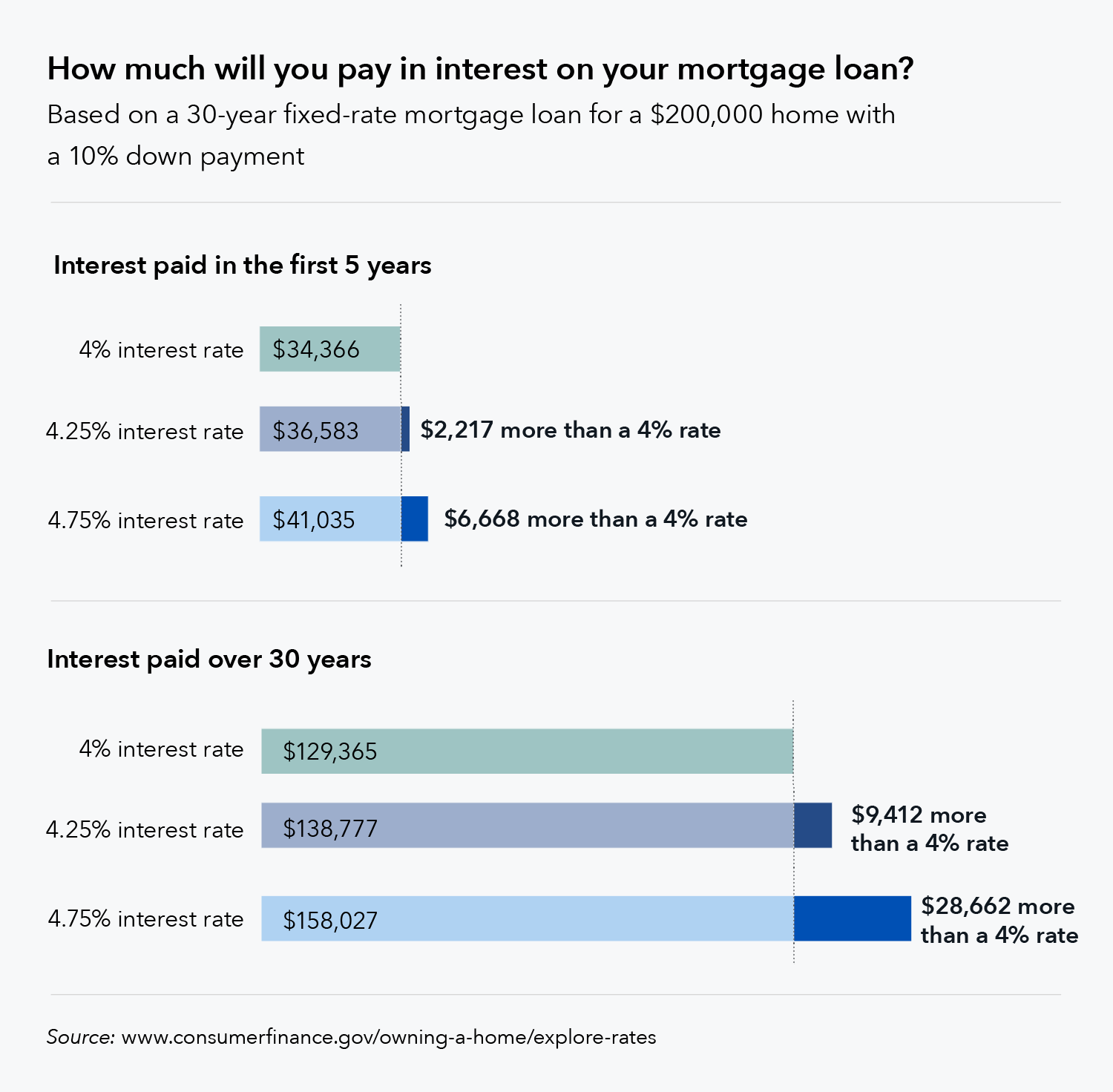

15 de octubre de 2024- What exactly do mortgage lenders select?

- Additional factors

- Tips alter your potential

Affiliate links into factors in this post come from partners one make up you (find all of our advertiser disclosure with your selection of couples for much more details). Although not, the views was our own. See how we speed mortgage loans to enter objective analysis.

- Minimal credit score that you’ll need pick a home may differ by financial and you will loan method of.

- It is possible to generally speaking you desire a credit history of at least 620 to possess traditional fund and 580 to have FHA fund.

- Down payment requirements are normally taken for zero to help you 20%, with regards to the loan system.

After you submit an application for a mortgage loan, lenders often remark your money and look to make sure you meet the requirements of one’s financing system. These can can consist of the absolute minimum credit rating otherwise a beneficial restrict financial obligation-to-money proportion.

The specific standards you will need to meet will vary of the mortgage sorts of, even when. This is what to know about qualifying to possess a mortgage.

Credit score

Of numerous home loan items are insured by government organizations. Thus, loan providers cannot accept borrowers having credit ratings underneath the minimal such teams set.

- Traditional financial: 620

- FHA mortgage: 580 that have an effective 3.5% down-payment or five hundred having a great ten% deposit

- USDA home loan: Nothing, but some loan providers wanted 640 or maybe more

It is important to say that lenders is actually liberated to put higher minimum credit score requirements than the borrowed funds-support teams need. Certain lenders might need the very least get away from 660 having old-fashioned fund, including.

Financing particular

Clearly above, per loan system possesses its own number of standards, therefore, the criteria you will have to see relies upon and this one you choose. Home financing elite group helps you determine which you’re best to your requirements.

Glance at and replace your credit history

The first step to boosting your score was finding out in which your stay. You could already look at your credit file at no cost after the week with all of around three biggest credit bureaus (TransUnion, Equifax, and you may Experian) during the AnnualCreditReport.

If you discover problems on the all of your reports, you can dispute all of them with the credit bureau including on the bank or credit card team. In terms of your credit score, the bank or bank card issuer may provide your own get to possess totally free. Or even, you can also have fun with a free credit score overseeing product for example Borrowing Karma otherwise Borrowing Sesame.

You might reduce your own bank card balances to reduce your borrowing usage rates. As well as, end trying to get people the latest kinds of borrowing when you look at the months before home financing app.

To start with, you ought to spend their bills timely every few days. Their payment records ‘s the component that has the most significant determine on your own credit history. Building a consistent reputation of to your-go out repayments will always be a surefire means to fix change your rating.

Improve your money otherwise reduce your debts

Incorporating an area concert, taking up longer at the office, otherwise requesting an improve is also the make it easier to be eligible for financing. Lowering your debts can also be, too how many installment loans can you have in Alabama.

Cut for a larger deposit

A larger down-payment means the financial institution should mortgage your less cash, that it can also generate being qualified easier. Even better, it could suggest all the way down rates as well.

Rating pre-acknowledged

Getting pre-recognized for the home loan doesn’t invariably help you be considered, however it is a sensible circulate prior to wanting a property. It does give you an idea of simply how much you could potentially borrow, exactly what rate of interest you will get, and you can what sort of monthly payment to expect. You may also use a mortgage qualification calculator to guage these wide variety.

Home loan credit history criteria Faq’s

It may vary of the financing types of, however, basically, a credit rating regarding 620 or maybe more is required for almost all old-fashioned mortgages. FHA fund succeed an effective 580 credit score that have a good step three.5% deposit (500 which have 10% down), whenever you are USDA and you will Virtual assistant funds lack official minimums. Lenders usually require 620 so you can 640 for these finance, though.

There’s no set count, your earnings are adequate to security your debt repayments while the advised mortgage payment conveniently. Based your loan program, the debt-to-income proportion must be below 41% so you’re able to 45%.

Sure, according to mortgage type of as well as your facts, you might be able to be eligible for a mortgage which have an excellent low if not zero down payment. Va funds, for-instance, don’t need a downpayment.

You can always implement again after cutting your DTI otherwise boosting your credit rating otherwise currently be eligible for home financing. To have mortgage loans, the criteria you’ll want to see confidence the loan system, thus there’s a chance switching the borrowed funds variety of you are making an application for may help, too.