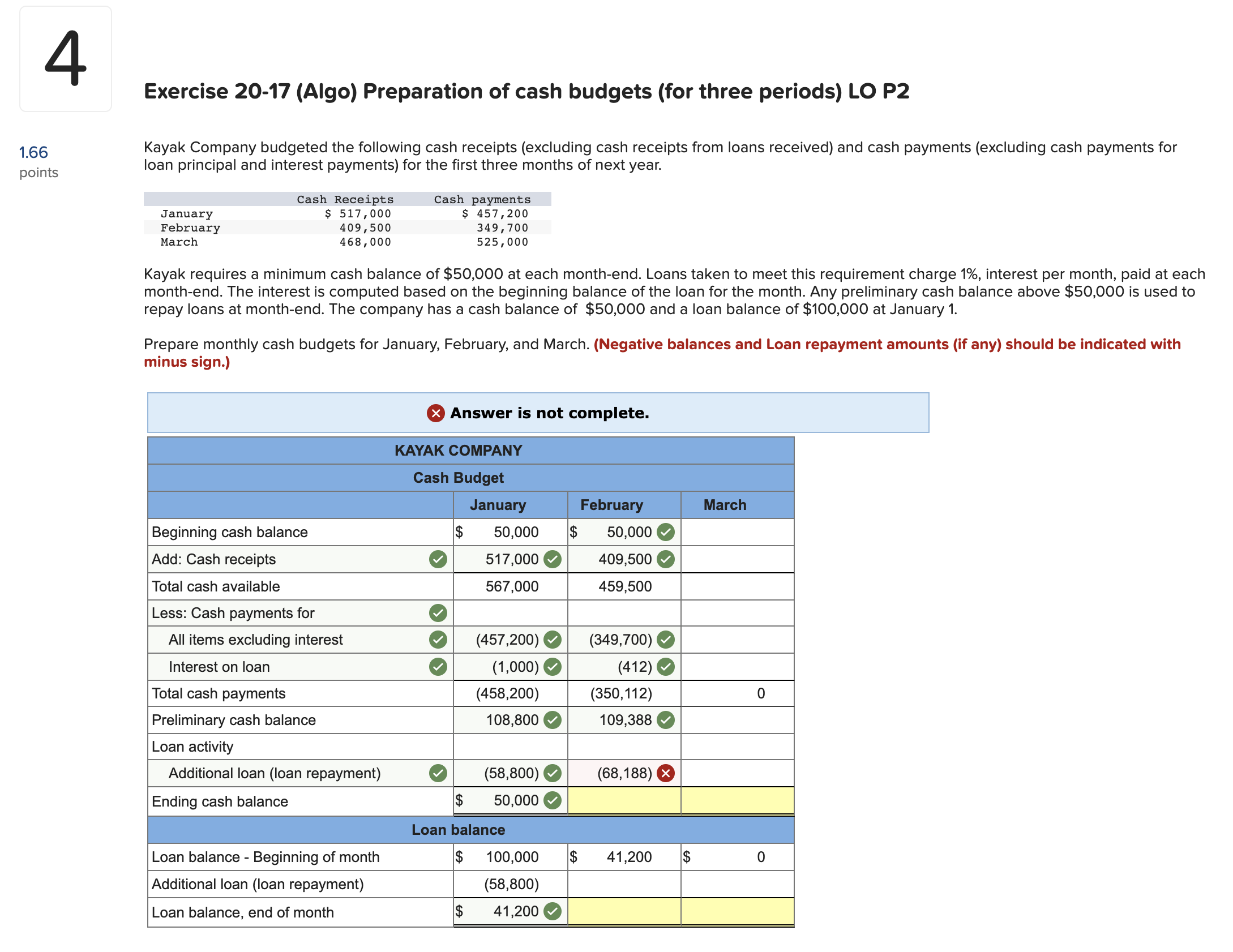

How does the borrowed funds be sure system really works?

7 de septiembre de 2024Investigation: Experts owed many from inside the refunds on Va home loans

7 de septiembre de 2024When you are desperate to pick a property but have no money to have a down payment, you may be lured to sign-to the for a no-down mortgage.

Because the notion of taking a new group of domestic tips in place of shedding any money at bank may seem tempting, there is usually a disadvantage to something this easy.

What are zero-off mortgages?

It should be come some time given that you’ve heard anyone explore zero-off home loans. This is because these include missing regarding marketplace for a little while, however, these are generally just starting to become popular again.

In other words, zero-down mortgage loans try money one to a hundred% fund the complete price of a house, getting rid of the necessity for a down payment.

Yes, you will find some finance that do not want a downpayment. However, observe: they are available having charges that get placed into the mortgage.

- Institution off Experts Factors Financing (Virtual assistant Fund), being designed for certified pros, active-responsibility solution embers, and certain members of the fresh Federal Guard and you may Supplies. Even though this loan needs no cash down, discover costs that will start from 1.25% to 3.3%.

- Service of Farming otherwise USDA’s Outlying Creativity financial be sure program. To be eligible for brand new USDA loan, you have to are now living in an eligible city, meet particular family earnings criteria, and be a first-go out homebuyer (though there are a handful of conditions). Like the Va mortgage, the brand new USDA how to get money loans fast loan is sold with charges. You will find a-1% up-front make certain fee and you may a yearly percentage away from 0.35% of your own loan harmony.

While doing so, there are several unique apps like the D that offers a zero-advance payment just in case you meet the requirements. Specific credit unions also provide these fund so you can users.

But more than likely, you will come across low-down fee financing that need one lay some cash down. The quantity you add down on these finance is as lower since the 1%, however, generally, you certainly will put step 3% so you can 5% off.

It’s also important to keep in mind that a lot of these money will need one hold private home loan insurance policies, otherwise PMI, that include hundreds on invoice.

What are the pros and cons out-of zero-money-down home loans?

Imagine being able to head into a financial instead of an all the way down percentage and go out towards keys to your brand new home. Audio fairly near to primary, proper? Yet not, there’s something you really need to look out for when you find yourself provided a zero-down mortgage.

When taking out a zero-off mortgage, you are susceptible to higher interest levels given that lender sees you because the «high-risk.»

Including, you end up capital a whole lot more. This requires you to spend more attention through the years. Put differently, for individuals who borrow more money right up-side, there will be a higher month-to-month mortgage repayment.

The most obvious pro from a no-down mortgage is the doorway they opens up if you’re unable to afford to get currency off. These types of home loan levels the new play ground and you can produces family possession more straightforward to to have if you have restricted financing and certainly will meet the requirements with a lender.

Whenever try a no-down financial an awful idea?

Even opting for one of many low-down commission fund is also make it easier to qualify for a lower life expectancy interest rate and higher conditions. As well as, you will lay aside many when you look at the attention and you may pay less cash over the life span of your financing.

A zero-off mortgage is actually an awful idea if you’re to buy a household into the a smaller-than-finest sector. I f you place no cash off and the field requires a nostrils-plunge, the worth of your property will go down (this is where the expression underwater is inspired by). You might find your self due more than you reside value.

Another reason to stop zero-off finance has to do with strengthening home collateral. For individuals who lay no money down in the very beginning of the loan, you will have no equity accumulated.

What makes that such as for instance an issue? Well, what if you really have a primary house crisis, just like your rooftop caving from inside the. When you have equity accumulated, you may be eligible for a property security financing otherwise a family collateral credit line (HELOC) to help you pay for the fresh new solutions.

However, strengthening collateral will take time and cash. For individuals who go for a zero-down loan it requires much longer to create guarantee.

When is a no-off mortgage wise?

A no-down home loan is actually put-as much as help you get towards a house if not have enough money secured to get on mortgage best away. Additionally it is best if you are planning to the becoming place for most many years.

However, prior to taking toward financing, be sure to have sufficient money into your finances to make this new monthly mortgage payments

Basically that it: it is best to lay some funds off because helps you to save you thousands ultimately.